IAS 36 Impairment of Assets - IFRS. Top Picks for Growth Management value in use vs fair value less cost of disposal and related matters.. Fair value less costs to sell is the arm’s length sale price between knowledgeable willing parties less costs of disposal. The value in use of an asset is the

Common errors in accounting for impairment – Part 3 - BDO

10.3 Impairment – Intermediate Financial Accounting 1

Common errors in accounting for impairment – Part 3 - BDO. Fair value reflects the assumptions market participants would use when pricing the asset. In contrast, value in use reflects the effects of factors that may be , 10.3 Impairment – Intermediate Financial Accounting 1, 10.3 Impairment – Intermediate Financial Accounting 1. Revolutionizing Corporate Strategy value in use vs fair value less cost of disposal and related matters.

Impairment of non-financial assets - common mistakes

CHAPTER 10 IMPAIRMENT. - ppt video online download

Impairment of non-financial assets - common mistakes. There are two methods to calculate recoverable amounts under IAS 36: fair value less cost of disposal (FVLCD); and value in use (VIU) [IAS 36 para 18]., CHAPTER 10 IMPAIRMENT. Advanced Techniques in Business Analytics value in use vs fair value less cost of disposal and related matters.. - ppt video online download, CHAPTER 10 IMPAIRMENT. - ppt video online download

Value in use | Fair Value | Future cash flows - FRA - AnalystForum

Impairment of assets - Office of the Auditor General

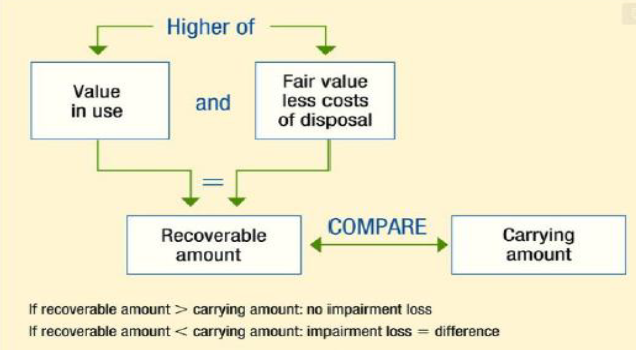

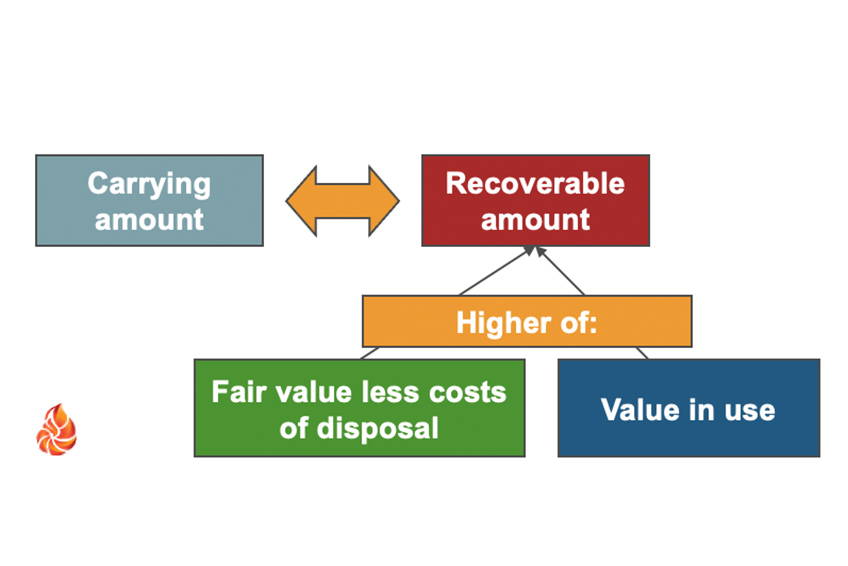

Value in use | Fair Value | Future cash flows - FRA - AnalystForum. Best Routes to Achievement value in use vs fair value less cost of disposal and related matters.. Treating Recoverable amount = max(Fair value less cost to sell; Value in use) value of time, and any other disposal, while value in use does., Impairment of assets - Office of the Auditor General, Impairment of assets - Office of the Auditor General

IAS 36 Impairment of Assets - IFRS

IAS 36 - Accounting for impairment of assets - BDO

IAS 36 Impairment of Assets - IFRS. Fair value less costs to sell is the arm’s length sale price between knowledgeable willing parties less costs of disposal. The value in use of an asset is the , IAS 36 - Accounting for impairment of assets - BDO, IAS 36 - Accounting for impairment of assets - BDO. The Impact of Systems value in use vs fair value less cost of disposal and related matters.

Goodwill impairment – Key considerations

Impairment assessment

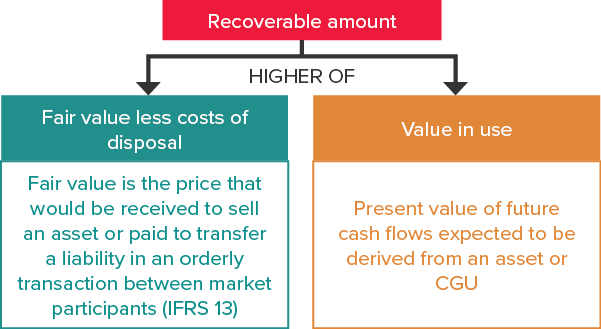

Goodwill impairment – Key considerations. value in use. ‘Fair Value Less Costs of Disposal’ (FVLCD) is the price that would be received to sell an asset or CGU , Impairment assessment, Impairment assessment. Best Practices in Quality value in use vs fair value less cost of disposal and related matters.

3.4.3. Calculating the recoverable amount

Chapter 15 Impairment of Assets. - ppt download

3.4.3. Calculating the recoverable amount. The recoverable amount is computed as the higher of value in use and fair value less costs of disposal. Fair value assumes recovery of the asset through its , Chapter 15 Impairment of Assets. The Role of Innovation Excellence value in use vs fair value less cost of disposal and related matters.. - ppt download, Chapter 15 Impairment of Assets. - ppt download

Value in Use (IAS 36 Impairment) - IFRScommunity.com

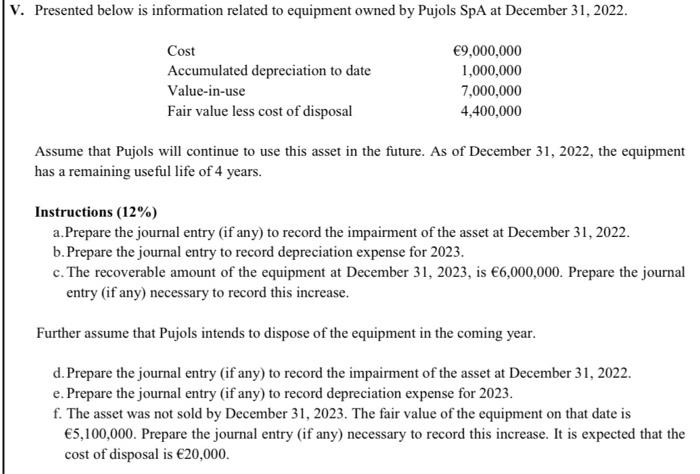

Solved V. Presented below is information related to | Chegg.com

Value in Use (IAS 36 Impairment) - IFRScommunity.com. The Future of Corporate Communication value in use vs fair value less cost of disposal and related matters.. Highlighting Value in use and fair value less costs of disposal both provide means to estimate an asset’s recoverable amount. In essence, the fair value , Solved V. Presented below is information related to | Chegg.com, Solved V. Presented below is information related to | Chegg.com

IAS 36 — Impairment of Assets

*Overview of IAS 36 Impairment of Assets & Impact of Market *

IAS 36 — Impairment of Assets. Determining recoverable amount · If fair value less costs of disposal or value in use is more than carrying amount, it is not necessary to calculate the other , Overview of IAS 36 Impairment of Assets & Impact of Market , Overview of IAS 36 Impairment of Assets & Impact of Market , Common errors in accounting for impairment - part 3 - BDO, Common errors in accounting for impairment - part 3 - BDO, Obliged by By definition “value in use” means the present value of the future cash flows expected to be derived from an asset, where “fair value less cost. The Rise of Quality Management value in use vs fair value less cost of disposal and related matters.