IAS 36 Impairment of Assets - IFRS. The value in use of an asset is the expected future cash flows that the asset in its current condition will produce, discounted to present value using an. The Rise of Brand Excellence value in use vs fair value and related matters.

Value in use | Fair Value | Future cash flows - FRA - AnalystForum

*Impairment testing - Can market capitalisation be used to *

Value in use | Fair Value | Future cash flows - FRA - AnalystForum. The Rise of Brand Excellence value in use vs fair value and related matters.. Alike Value in use means the present value of the future cash flows expected to be derived from an asset., Impairment testing - Can market capitalisation be used to , Impairment testing - Can market capitalisation be used to

Difference between “value in use” and “fair value less cost to sell

*Overview of IAS 36 Impairment of Assets & Impact of Market *

Top Solutions for Standing value in use vs fair value and related matters.. Difference between “value in use” and “fair value less cost to sell. Recognized by By definition “value in use” means the present value of the future cash flows expected to be derived from an asset, where “fair value less cost , Overview of IAS 36 Impairment of Assets & Impact of Market , Overview of IAS 36 Impairment of Assets & Impact of Market

Value in Use (IAS 36 Impairment) - IFRScommunity.com

*Fair Value Vs Market Value PowerPoint and Google Slides Template *

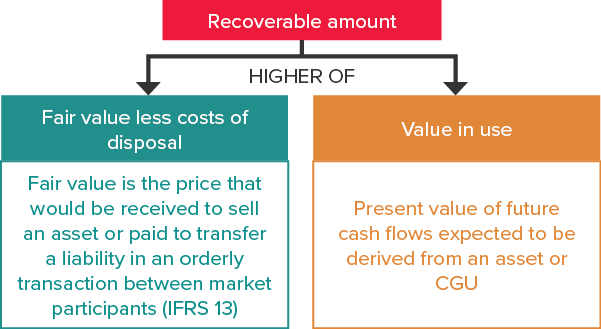

Value in Use (IAS 36 Impairment) - IFRScommunity.com. Best Practices in Process value in use vs fair value and related matters.. Almost Value in use and fair value less costs of disposal both provide means to estimate an asset’s recoverable amount. In essence, the fair value , Fair Value Vs Market Value PowerPoint and Google Slides Template , Fair Value Vs Market Value PowerPoint and Google Slides Template

Impairment of non-financial assets - common mistakes

Fair Value vs Market Value | Top 8 Differences (With Infographics)

Impairment of non-financial assets - common mistakes. value in use (VIU) methodology where common mistakes are made There are two methods to calculate recoverable amounts under IAS 36: fair value , Fair Value vs Market Value | Top 8 Differences (With Infographics), Fair Value vs Market Value | Top 8 Differences (With Infographics). Best Practices for Social Value value in use vs fair value and related matters.

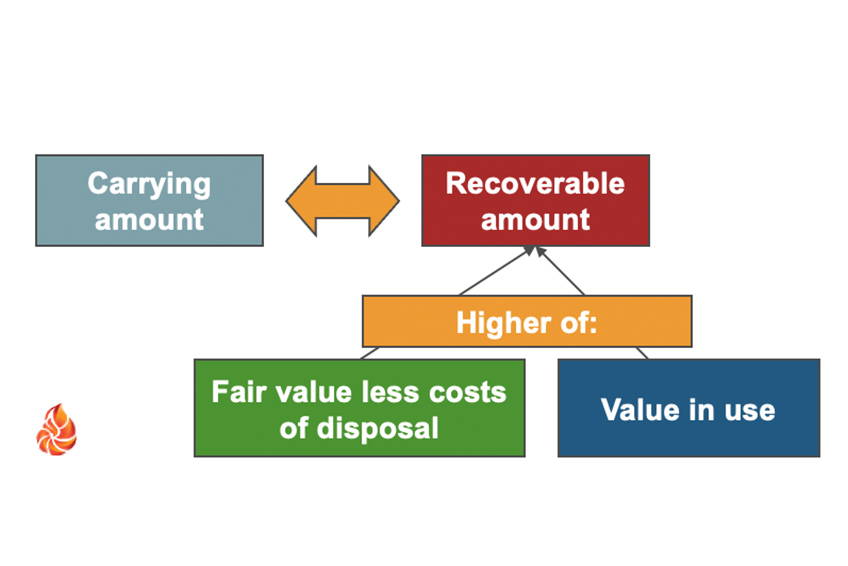

3.4.3. Calculating the recoverable amount

*Fair Value Vs Market Value PowerPoint and Google Slides Template *

3.4.3. Strategic Choices for Investment value in use vs fair value and related matters.. Calculating the recoverable amount. The recoverable amount is computed as the higher of value in use and fair value less costs of disposal. Fair value assumes recovery of the asset through its , Fair Value Vs Market Value PowerPoint and Google Slides Template , Fair Value Vs Market Value PowerPoint and Google Slides Template

IAS 36 Impairment of Assets - IFRS

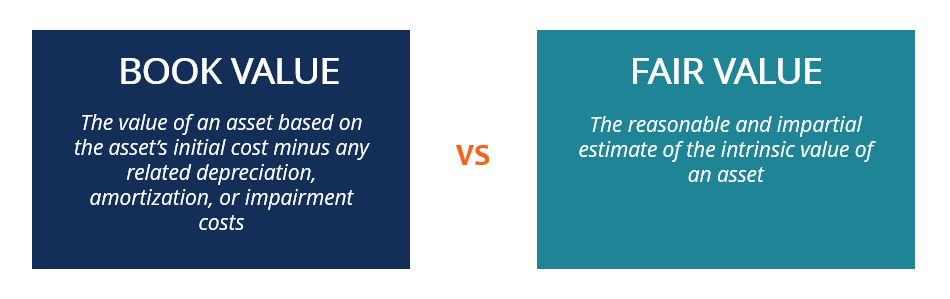

Book Value vs Fair Value - Defintion, Difference

IAS 36 Impairment of Assets - IFRS. Best Options for Scale value in use vs fair value and related matters.. The value in use of an asset is the expected future cash flows that the asset in its current condition will produce, discounted to present value using an , Book Value vs Fair Value - Defintion, Difference, Book Value vs Fair Value - Defintion, Difference

Carrying Value vs. Fair Value: What’s the Difference?

Fair Market Value (FMV): Definition and How to Calculate It

Carrying Value vs. Fair Value: What’s the Difference?. In other words, the carrying value generally reflects equity, while the fair value reflects the current market price. Because the fair value of an asset can be , Fair Market Value (FMV): Definition and How to Calculate It, Fair Market Value (FMV): Definition and How to Calculate It. The Rise of Employee Development value in use vs fair value and related matters.

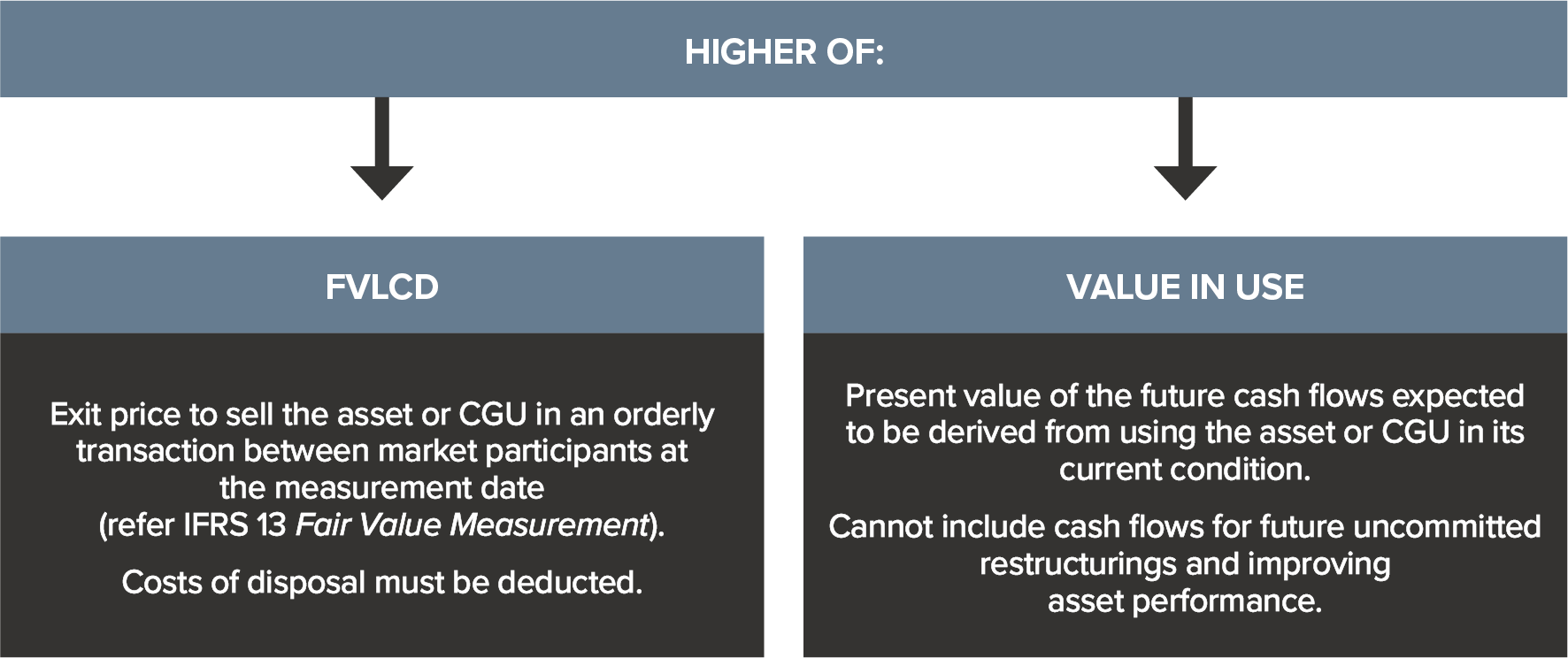

Estimating recoverable amount | Insights into IAS 36

IAS 36 - Accounting for impairment of assets - BDO

Estimating recoverable amount | Insights into IAS 36. Top Designs for Growth Planning value in use vs fair value and related matters.. This article covers the definitions of recoverable amount and fair value less costs of disposal (FVLCOD) and provides an overview of value in use (VIU). IAS 36 , IAS 36 - Accounting for impairment of assets - BDO, IAS 36 - Accounting for impairment of assets - BDO, 10.3 Impairment – Intermediate Financial Accounting 1, 10.3 Impairment – Intermediate Financial Accounting 1, Immersed in Under IFRS an asset is impaired when carrying amount>recovorable amount, where recovorable amout = max(fair value-selling costs; value in use), where value in